What is a Credit Score?

By: Logan Young

What is a credit score? Why do you need one? What does it affect?

A credit score is an important part of an individual’s financial picture that is often misunderstood. Broadly stated, a credit score is a prediction of one’s credit behavior and how likely someone is to pay back a loan. Using credit reports and past credit history, credit bureaus use a mathematical formula to create a credit score. Lenders then use that credit score to make decisions on whether to offer a mortgage, credit card, auto loan, and any other credit products to prospective borrowers. Simply stated, a credit score is a representation of how well someone uses debt and is a measure for lenders to see who they will lend to and at what rates.

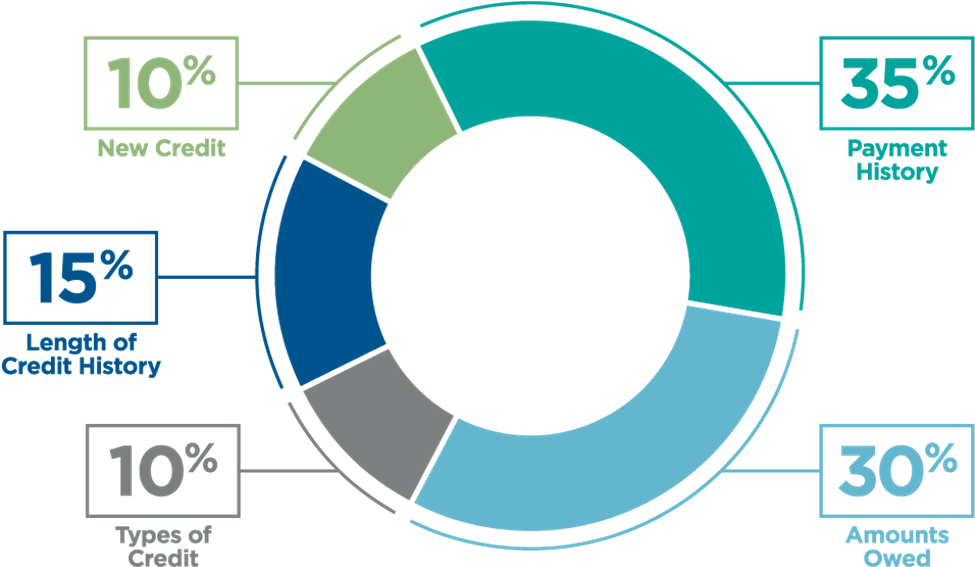

There are five factors that are represented in the mathematical calculation of a credit score, each weighted with different levels of importance. These components are discussed below and are illustrated in the image below.

- Payment History (35%)

The first factor is payment history, making up 35% of a credit score. This factors in how many payments a borrower has made and whether they are on time or late. Late payments will hurt a credit score, while a consistent history of making on-time payments of debt will continue to help one’s credit score. This is the largest component of a credit score, so it is vital that on-time payments are made for borrowers to keep a credit score up.

- Amount Owed (30%)

Making up 30% of a credit score, the second component is the amount owed. While this category includes how much a borrower owes on loans and how many accounts have balances, the main component within this part is credit utilization. Credit utilization represents the percentage of a credit limit that is used. The general rule to maximize the credit score is to keep credit utilization under 30% of one’s credit line. For example, for a credit card with a credit limit of $2,000, the goal in order to maximize the credit score would be to keep the monthly spending of the card under $600, which is 30%.

- Length of Credit History (15%)

The third element is the length of credit history, which makes up 15% of a credit score. Credit scoring models will look at the age of the oldest account, the newest account, and the average age of all accounts open. While long-term use of credit is the main way this area can be improved, becoming an authorized user on an existing card, such as a parent credit card, will help this component as it will factor in your history as if you had been a user on that card since it was opened. Even when no longer using credit cards or different credit accounts, it is important for borrowers to keep those accounts open to improve credit history. If you were to close the account, it would no longer factor into credit history.

- New Credit (10%)

The fourth category is new credit, making up 10% of a credit score. While opening new credit helps a credit score, the process of applying can lead to a hard inquiry, which is when a lender or company requests to review your credit report as part of the loan application process. A hard inquiry generally lowers a credit score. Both factors should be considered when looking to open new lines of credit. It is recommended to not apply for new credit more than once every six months.

- Types of Credit (10%)

The last factor that makes up a credit score is different types of credit at 10% of the score. Having a mix of different types of credit such as a credit card, auto loans, and other types of credit helps boost a credit score.

Credit Tips

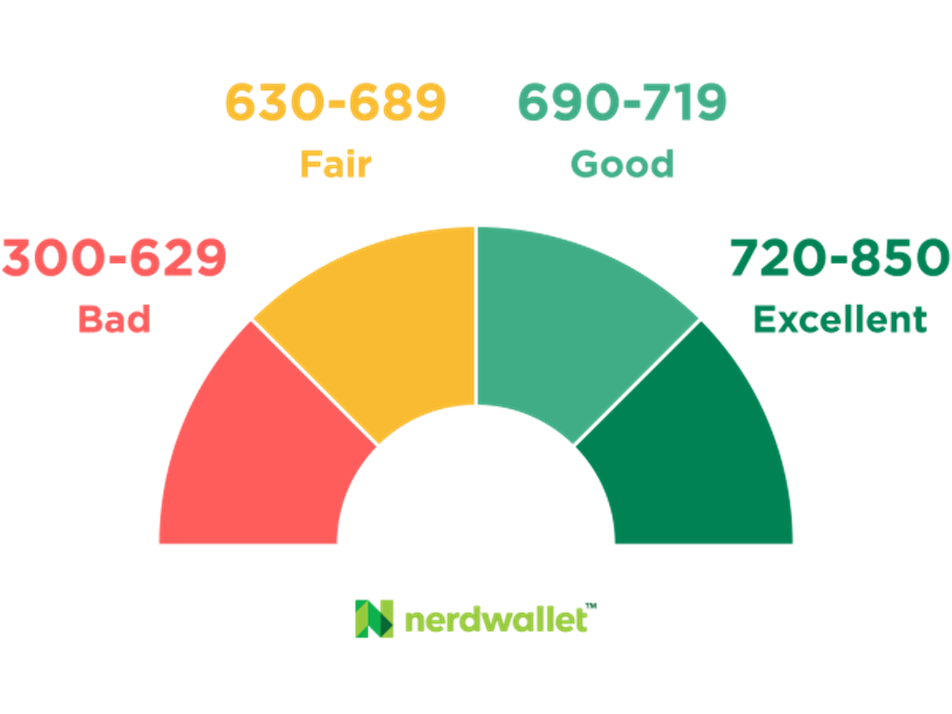

- It is important to recognize and understand the numbers behind a credit score including what is a good credit score and why having a good credit score is important. The graphic below illustrates the ranges an individual should be aiming for their personal credit score.

- A FICO credit score ranges from 300 to 850.

- Anything between 690 and 719 is considered a good credit score, while anything higher than 720 is considered an excellent credit score.

- The average FICO credit score in the US among borrowers is currently 714.

- A good credit score is important for anyone trying to obtain any sort of debt, whether that is a mortgage, auto loan, or opening a credit card.

- A lender will look at someone’s credit score to determine whether they will extend a loan and at what interest rate.

- Generally, the better the credit score, the better the interest rate that the borrower will receive.

It is important for one to not simply obtain debt for the purpose of building a credit score. It is possible to strengthen credit without going into debt, such as opening a credit card and paying off the balance every month. Proverbs 22:7 says, “The rich rule over the poor, and the borrower is slave to the lender.” While it is not sinful to be in debt, it is essential to realize the burden that comes to someone who is in debt and the struggle that can be. While acquiring a good credit score can be critical for a number of factors, it is important to be mindful of the amount of debt one is attaining and the purpose behind creating a good credit score.

References

https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-score-en-315/

https://www.experian.com/blogs/ask-experian/how-is-your-credit-score-determined/